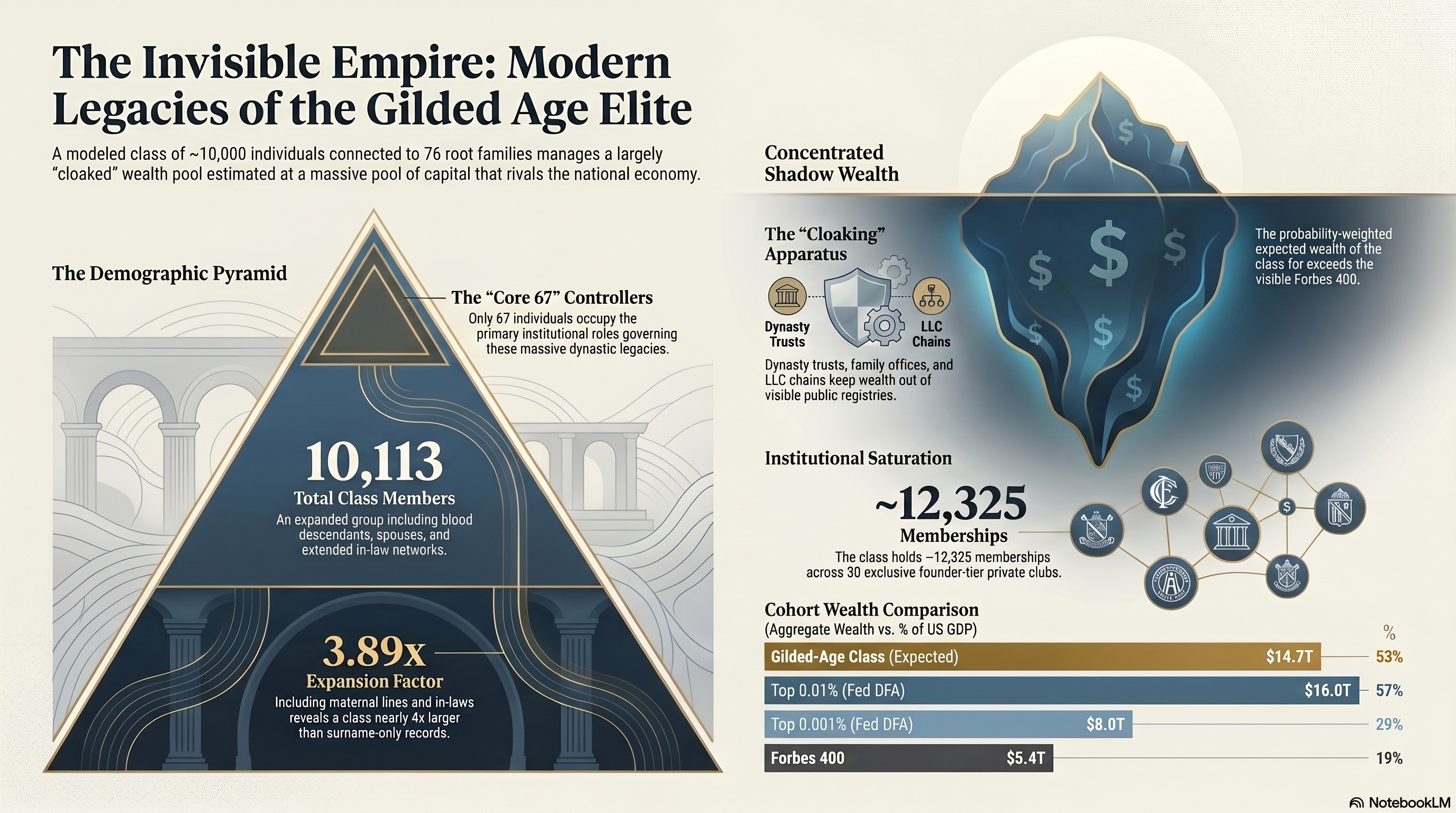

30 clubs across 11 metros.

Class-share = estimated fraction of total members traceable to the

modeled class. Aggregate class-tied seats = 12,325.

Knickerbocker Club NYC 1871 1,000 45% 450

Union Club of the City of New York NYC 1836 1,500 35% 525

Metropolitan Club NYC 1891 1,800 30% 540

The Brook NYC 1903 500 50% 250

Racquet and Tennis Club NYC 1890 1,700 30% 510

The Links Club NYC 1916 1,100 35% 385

River Club of New York NYC 1931 750 35% 263

Century Association NYC 1847 2,300 20% 460

New York Yacht Club NYC 1844 3,000 20% 600

Somerset Club Boston 1851 1,000 50% 500

Union Club of Boston Boston 1863 1,400 35% 490

The Country Club Boston 1882 1,300 45% 585

Tavern Club Boston 1884 700 30% 210

Philadelphia Club Philadelphia 1834 800 50% 400

Rittenhouse Club Philadelphia 1875 500 30% 150

Chicago Club Chicago 1869 1,300 40% 520

Casino Club Chicago 1914 1,000 40% 400

Onwentsia Club Chicago 1895 700 45% 315

Pacific-Union Club San Francisco 1852 900 45% 405

Bohemian Club San Francisco 1872 2,700 20% 540

Burlingame Country Club San Francisco 1893 700 45% 315

California Club Los Angeles 1887 1,800 30% 540

Metropolitan Club (DC) Washington DC 1863 2,400 20% 480

Cosmos Club Washington DC 1878 3,300 15% 495

Bailey's Beach Club Newport 1897 450 60% 270

Reading Room Newport 1854 300 60% 180

Bath & Tennis Club Palm Beach 1926 1,200 45% 540

Everglades Club Palm Beach 1919 800 45% 360

Maidstone Club East Hampton 1891 950 45% 428

National Golf Links of America Southampton 1911 400 55% 220